Blockchains and smart contracts

Dr. Daniel Burgwinkel is a partner in the Records Management competence center and has more than 15 years of project and research experience in the field of smart contracts. He holds a PhD from the University of St. Gallen.

The fintech community is absorbed in discussions of the possible future applications of blockchain technology. What kinds of blockchain platforms are already under development and what potential do they have?

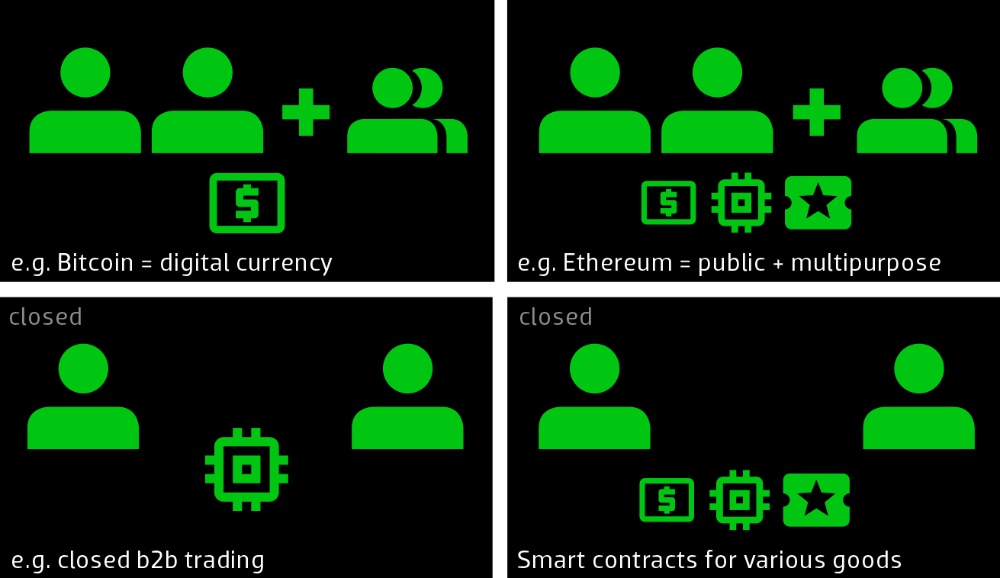

Types of blockchain platforms: left, blockchains with one use case; right, blockchains with multiple use cases

Types of blockchain platforms: left, blockchains with one use case; right, blockchains with multiple use cases

The term blockchain refers to a technical concept whereby data is not stored in a central database, but on users’ decentralized systems using encryption. The word ‘blockchain’ was chosen because the data is stored in individual blocks, which are then distributed across the network participants’ systems, while the order of the blocks is documented using a chain concept.

Although this is only a technical concept, experts believe that this approach will revolutionize business models in all manner of industries – including finance.

A look at the business models of today’s electronic marketplaces, like stock exchanges or internet auctions, reveals how sellers and buyers use a central authority to manage the purchase and settlement process – like a stock exchange or auction platform. The operators of such platforms coordinate the sales process and ensure the smooth flow of business.

The main innovation in applications that use blockchain technology is that buyers and sellers are able to interact directly with one another. They no longer need a centralized operator to control the purchasing and settlement process or ensure that the buyer receives what they paid for and that the seller receives the money. In an electronic market place based on blockchain technology, the sales contract is stored in the blockchain using digital encryption methods that make it possible to detect if the contract had been manipulated. The program codes stored in the blockchain then automatically examine the conditions of the contract, e.g. if the buyer has already paid for the product or service.

Bitcoin – the first blockchain revolution

Currently, the best-known use of blockchain technology is the digital payment network Bitcoin, which was founded in 2009. Participants can exchange payments made using the Bitcoin cryptocurrency directly with one another and do not need to involve any traditional banks. The payment information is distributed across the participants’ systems using the blockchain method. Every completed transaction can therefore be tracked in the register of the Bitcoin blockchain, which shows that user A has transferred X amount to user B. Unlike traditional payments, participants do not have to give their real identity. Rather, they can use a pseudonym in place of their real name. It has become clear that blockchain technology, especially the idea of distributed data storage, can be applied to other scenarios.

Blockchain – more fintech hype?

Various open source and commercial software projects use blockchain technology and the people behind them are looking for appropriate fields of application. Banks and IT companies reveal new blockchain projects every week. For example, Goldman Sachs reported in December 2015 that they intend to use blockchain technology for digital securities trading, and Microsoft is offering blockchain applications through its cloud services. At the end of 2015, the Linux Foundation announced that it wants to develop an open source blockchain standard in cooperation with users and technology companies.

The blockchain approaches used by non-banks threaten financial institutions’ established business models. This is why the banks’ fintech incubators are feverishly attempting to mark out various territories before start-ups seize these opportunities.

On the one hand, blockchain technology could be used to build low-cost alternatives to cash or trading systems. In 2015, more than twenty global banks worked together to form an initiative to drive forward development, the R3 CEV consortium.

On the other hand, blockchain technology can be used to realize entirely new use cases, such as the handling of digital contracts, innovative methods for the official recording of business-related information, or the storage of sensitive health data.

Open and closed blockchain platforms

Blockchain platforms can be split into two categories. First there are the open platforms, also referred to as public blockchains, where any user can register and start using the services. Then there are closed networks, private blockchains, where only defined participants, such as companies in a particular industry consortium, are granted access.

The Bitcoin network is a public blockchain. This means that new users can join the Bitcoin network. There are also use cases for private blockchains, such as using blockchains in a closed industry network.

A further subdivision of blockchain applications can be made based on the intended use. Here it is possible to differentiate between blockchains that have precisely one application and blockchains which can be used for a variety of purposes.

The blockchain approach is used for a dedicated purpose in the Bitcoin network, specifically the creation of a digital currency (single purpose). One example of a blockchain platform that can be used to realize a wide variety of use cases is the Ethereum initiative, which was founded in 2014 as a non-profit organization and is based in Zug near Zurich. Ethereum provides a blockchain and the accompanying software that participants can use to develop their own programs and smart contracts for various purposes.

Smart contracts

Contractual agreements between two or more parties can be saved in a blockchain and processed digitally from start to finish. A digital contract documents the agreement between the involved parties, for example for the purchase of a digital product. The contractual clauses are documented in the blockchain in a machine-readable format and can then be executed by the computer system using established rules immediately upon entering into an agreement. The Ethereum network supports smart contracts. Contracts like this are particularly interesting for businesses where the buyer and seller do not know one another, like in the case of short-term apartment rentals. This could allow smart contracts to compete with established online players like airbnb.

Digital notaries of the future could use blockchain technology to notarize ownership status, e.g. land registry entries. There are already projects underway where people hope to use blockchains to establish land registries in developing countries, like Honduras.

Conclusion and outlook

There is a spirit of optimism among startups when it comes to blockchain technology, because several players have been able to acquire venture capital within a short space of time. Around twenty startups in this field were awarded 80 million dollars in the last quarter of 2015 alone. Partnerships with global software providers like Microsoft and the Linux Foundation have also shown that established technology providers are taking the concept of blockchains seriously. Global banks, too, have caught onto the idea. The large number of potential applications also shows that blockchains and smart contracts have the potential to do more than just turn the banking and insurance industries on their head: these concepts could be used to generate new business models in every sector. But this requires that sustainable use cases can be identified and that blockchain technology can meet performance and security requirements. Blockchains could be especially useful in business-to-business transactions, making it possible to create networks for digital contracts that were not previously covered by traditional EDI (Electronic data interchange) or business-to-business market places.

Advantages of blockchain technology based on a figurative example

Suppose an environmental organization would like to form a global network for measuring and securely recording the exhaust emissions of diesel vehicles. The reason being that the manipulation of exhaust emissions test results by car manufacturers has shattered consumers’ trust. The environmental organization would like to demonstrate how the community can make objective facts accessible to all via a distributed network on a blockchain platform. Measured values can be tested every time a car goes in for service – completely independently of official measurements. Each participant would measure these values effectively for themselves and then publish the results online in the blockchain. A smart contract would then examine the data submitted and generate an alert if the values recorded exceed acceptable limits.

In this example, the organization would be able to create the network relatively quickly on an existing blockchain platform like Ethereum and would not need to invest in a central server in a highly secure data center. Using blockchains also ensures the integrity and availability of the data, as data cannot be altered by third parties at a later date. Every transaction – i.e. every entry of recorded data – can be tracked and monitored through the system.

Which use cases will be successful?

The real innovative power of blockchain technology only becomes clear when you look at specific applications. The following questions are helpful when evaluating a blockchain use case:

- Who are the participants in the network and how do the end users benefit from the blockchain technology?

- How do network participants interact and what roles (buyer, seller, etc.) can they have?

- What is the focus of the application? Is it a digital currency? A contract? Or is it used to authenticate transactions?

- Why do participants want to use blockchains rather than a traditional technology? What advantages are there to cutting the previous central authority out of the equation, where it used to coordinate market participants and ensure trust? What business model are the founders of this blockchain-based marketplace following?

- How does blockchain offer technical advantages in this use case?

- Why will this blockchain application succeed? Will this use case be an alternative to traditional approaches or does it offer an entirely new benefit?