Quantities matter – even in Switzerland

Christian Walter ist Geschäftsführer und Redaktionsleiter von swiss made software. Bis Ende 2010 arbeitete er als Fachjournalist für das ICT-Magazin Netzwoche, publizierte zuletzt aber auch im Swiss IT Magazin, der Computerworld sowie inside-it.

Asking for money online – whether it’s for a CD, a good cause, in exchange for interest or a share in a company – that’s crowdfunding, and the field has grown far beyond the confines of philanthropy. But not everyone knows it – including the regulator.

Crowdfunding has become more than plain philanthropy. But not everyone knows it – including the regulator. (© Miriam Dörr/Fotolia)

Crowdfunding has become more than plain philanthropy. But not everyone knows it – including the regulator. (© Miriam Dörr/Fotolia)

Crowdfunding is booming – especially outside of Switzerland. Worldwide growth was 167 percent in 2014, with a total volume of 16.2 billion dollars. Definitive figures for 2015 have not been released as of the time of writing, but market researchers Massolution are talking about the figure doubling to 34.4 billion dollars. A completely new global industry has emerged, although Switzerland is lagging slightly behind the trend. The total volume of crowdfunding in Switzerland was a mere 15.8 million francs in 2014, according to the ‘Crowdfunding Monitoring’ study produced by the Lucerne University of Applied Sciences and the Arts. Growth was a ‘mere’ 36 percent.

This is of course very ‘Swiss’. Particularly in the b2c sector, it is not unusual for pioneering new IT-based business models to be developed abroad and only arrive in the Swiss cantons once many basic questions relating to the business model have already been cleared up. This is not only down to Swiss caution. The Swiss market is also quite small, and it is much harder to achieve economies of scale than it is in countries like Germany, the United States, or China. The regulator, too, has an inhibitory effect. From the perspective of the crowdfunding industry, FINMA only really started concerning itself with the fintech sector, to which crowdfunding belongs, in 2015. Despite initial talks, crowdfunding start-ups continue to find themselves in a legally uncertain environment.

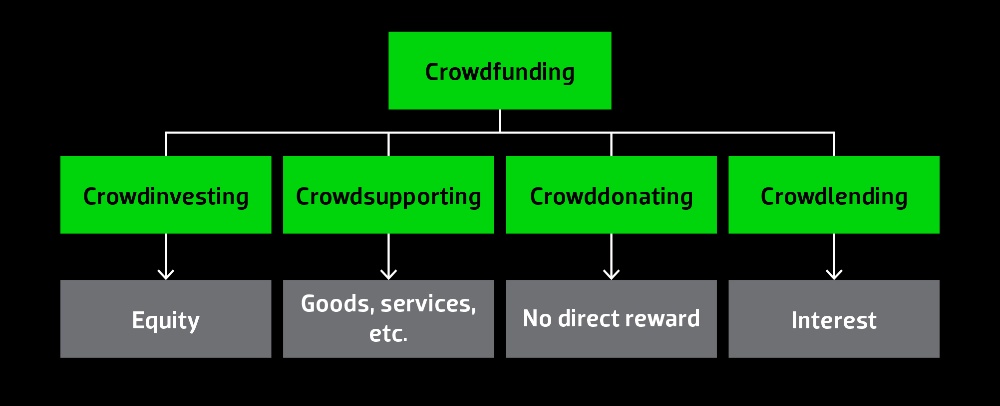

It is nothing new for a regulator to be unable to keep up with the dynamics of the market. And fintech is a demanding field – not least because the term is notoriously vague. Even in crowdfunding there is a variety in the exact set of challenges businesses face, because just like fintech itself, the term refers to a wide range of different business concepts. These include ‘crowddonating’ (normal online donations), ‘crowdsupporting’ (donations given in exchange for something, e.g. a CD, book, or game), ‘crowdinvesting’ (investment in commercial enterprises), and ‘crowdlending’ (lending of money to private individuals or businesses by other private individuals or businesses).

Many ways to work the crowd

Something all forms of crowdfunding have in common is that they make it possible to fund campaigns through the internet, bringing together a multitude of people for cultural, social, or commercial projects. Communication between investors and borrowers is mediated by internet-based intermediaries – crowd-funding platforms. The intermediaries are compensated through fees that are generally based on a percentage of the amount collected. Investors are compensated either monetarily or through other means, depending on the type of crowd-funding.

Currently all the forms of crowdfunding listed above are experiencing very high growth rates. That said, progress in each individual area differs greatly depending on the country. The best known and certainly the lead initiator of this movement is crowdsupporting, with its internationally renowned exponents like Kickstarter and Indiegogo.

Switzerland has similar platforms like 100Days or Wemakit. The ‘investor’ supports a project, like a CD or book, and then receives a one-off reward in the form of products, artistic works, or services. Together with crowddonating, the classic online donation system, this is the largest crowdfunding sector in Switzerland. After only 300,000 francs were collected in 2011, this sum had already grown to 7.7 million by 2014. That is remarkable, but still lagging behind development in the rest of the world. A study by the University of Cambridge examined the situation across Europe: examining the whole of Europe while excluding the United Kingdom, one sees a total investment of 120.3 million euros, with a growth rate of 127 percent. The United Kingdom alone had another 34 million.

The fact the Brits are storming ahead of their European competitors is easy to identify through a look at the local market. The United Kingdom contributes 2.34 billion euros of the almost 3 billion euros that make up the total volume of the European crowdfunding market – an incredible 74.3 percent. The number of Brits among the numbers of service providers shares a similar lead. With 65 platforms, they are at the top and ahead of Spain (34), France (33), Germany (31) and the Netherlands (31). Still - Switzerland is not doing badly with just under 30 different providers.

Forms and rewards in different forms of crowdfunding

Forms and rewards in different forms of crowdfunding

Each country to its own

The largest part of the British crowdfunding sector is crowdlending, with leaders such as Zopa, Ratesetter, or Funding Circle. This allowed almost a billion euros to be loaned to small and medium-sized enterprises in 2014. Growth was 253 percent. The next-largest is crowdlending, whereby loans are granted to private parties, which hit a volume of 752 million euros or a growth of 113 percent. With a volume of 274.6 million, this is actually the top category in the rest of Europe, while business lending is in third place with 93.1 million (272 percent). Crowd-supporting, as mentioned above, finds itself in second place.

Interestingly, there had not yet been any form of crowdlending for SMEs in Switzerland by 2014. Only private individuals were able to receive loans through crowdlending, and even then, the total only amounted to 3.5 million francs, which is almost twice the sum for the previous year. At 85 percent, this is one of the fastest-growing forms of crowd-funding in the Swiss crowdfunding sector. In fact, Cashare, a crowdlending platform founded in 2007, was the first ever crowdfunding platform altogether.

A considerable six years lie between the founding of the first crowdfunding platform in Switzerland and the founding of the first crowdfunding worldwide. ArtistShare, founded in 2001, is often reported as being the first such platform, while the most well-known international exponents, Indiegogo and Kickstarter, followed in 2008 and 2009 respectively. All three are classed as crowdfunding platforms.

The regional differences can also be observed in the relationships with regulators. The president of the UK Crowd-funding Association (UKFCA), Bruce Davis, is of the opinion that the Brits now have exceptionally great regulations which are perfectly tailored to the needs of this industry. In France, too, there are regulations that are specially designed to suit the needs of the crowdfunding sector, and these were designed in cooperation between both the industry itself and its regulators. The same also applies to the United States. “Switzerland must create a legal framework for these platforms that is adapted to the nature of their existence. The current situation makes it almost unilaterally impossible or at least very difficult to unleash the full potential of crowdfunding for both business and society,” says Hannes Gassert from Wemakeit.

Swiss peculiarities and problems

A good example of typical Swiss problems what is known as the twenty-percent rule in crowdlending. In Switzerland, only a maximum of 20 people are permitted to contribute money to any one project unless the intermediary is a bank. To exceed this number, platforms would be forced to acquire a banking license, which is no easy feat in Switzerland. Currently the industry is making do with a variety of workarounds. Nevertheless, certain business models that have worked abroad cannot be emulated in Switzerland.

The final major form of crowdfunding is crowdinvesting, which has a volume of 4.6 million francs in Switzerland. Here it is less about a particular project, and more about making an investment in a company in the form of equity or mixed forms of equity and debt capital (mezzanine capital), usually start-ups. However, in 2014 the invested sum fell around 18 percent from 5.6 million the previous year. According to Crowdsourcing Monitor, people should not pay too much attention to the change in volume “due to the very low number of projects.”

Switzerland is trailing behind in more than just volume. This can be seen in the development of business models, which at the moment continues to take place largely abroad. One good example here is US-based InvestUP. This company makes it possible to access various lending and funding platforms in one place and also offers an ‘auto-invest’ function. First risk profiles are created, then InvestUP invests the available funds in appropriate loans for individuals or companies on various platforms. Once loans are repaid, the money is automatically reinvested in new loans.

The previously mentioned twenty-percent rule makes such a business model as good as impossible in Switzerland. At InvestUP, the risk is minimized by distributing invested funds in the form of numerous micro-investments. The aforementioned twenty-percent rule forces individual investors to invest significantly higher amounts, as each loan must be supported by a smaller number of investors.

FINMA will need to take action here, otherwise the platforms and associated business will probably head elsewhere. Legal security is also a serious concern in other forms of crowdfunding. One such form is crowdinvesting, which some industry insiders are touting as a great financing option for start-ups. Should the current growth continue, then this form of financing could expand from its current one-billion-dollar volume in the United States to 26 billion dollars by 2020.

The new venture capitalists

The total volume of venture capital in the United States was 48.3 billion dollars in 2014, according to the PWC Money Tree Report. This, however, is a record, and annual investments have usually totaled around 30 to 40 billion dollars throughout the past decade. If crowdinvesting continues to develop according to projections, then this could represent a viable alternative to traditional venture capital.

Even if these projections are a little over-enthusiastic, it would still be very sensible for Switzerland to develop these channels. It is an unfortunate fact that it is hard for Swiss start-ups to find money. That is not to say Switzerland finds it hard to innovate. The country has also seen some interesting developments of its own – for example, the Basellandschaftliche Kantonalbank was the first bank to open a crowdfunding platform. This is a software-as-a-service platform provided in cooperation with Swisscom. The Luzerner Kanonalbank and Raiffeisen Bank plan to follow with their own platforms in 2016. And so it seems we have something almost unique happening here in Switzerland. “With just a few exceptions, banks in Europe do not have their own platforms,” says Andreas Page of Swiss-com. “It is up to each bank to decide for itself whether it would be more successful to run its own platform or collaborate with an existing platform.”

Crowdfunding is booming. And various studies agree that it will continue to boom over the coming years. Which forms of crowdfunding will take off in Switzerland depends heavily on the upcoming decisions to be made by FINMA. Either way, fintech and crowdfunding are now definitely on the agenda, and there is now an ongoing dialogue with the industry at large. “Organizations such as the Swiss Crowdfunding Association, Swiss Finance Start-ups, and Swiss FinteCH have given the industry its own representative bodies. This also makes FINMA’s job easier. Now they have points of contact who are easier for them to work with than a diverse bunch of entrepreneurs,” says Hannes Gassert of Wemakeit. Europe, too, needs to think seriously about its future. In 2014, Asia achieved a market volume of 3.4 billion euros, overtaking Europe, which only made 3.26 billion euros. In spite of this, a large part of this market is still very much based in the United States. Here, almost 60 percent of the entire market, or 9.46 billion dollars, were generated in the same year.

One thing is clear: this promising sector still has a lot of potential to fulfil, both within Switzerland and abroad.